News & Articles The difference between now and 1998

The difference between now and 1998

8 Aug 2015

THE ringgit is falling and so is the stock market. Contagion worries are building.

That scenario is a reality for Malaysian capital markets and the anxiety over a slowdown in China’s economy has got many worried about its effect on economic momentum in Malaysia.

Parallels from such a situation today can be drawn against what happened during the Asian Financial Crisis of 1997/98 but the setting is different than what happened almost 20 years ago.

Going back to 1997/98, it was a time when growth in Malaysia and South-East Asia was booming. Overheating worries turned into whether such growth was sustainable.

Starting with the attack on the Thai baht, the currencies of many South-East Asian countries were soon under attack.

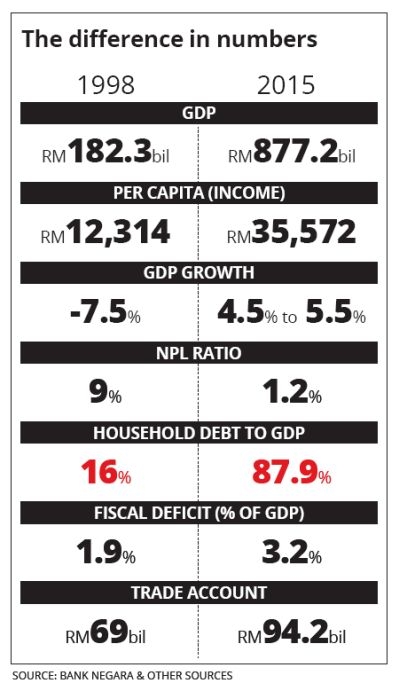

The ringgit too felt the brunt of such attacks and at the worst, fell to RM4.80 to the dollar before recovering and ultimately pegged at RM3.80 to the dollar in September 1998.

“In 1997/98, it was contagion that caused problems. The currency crisis turned into a financial crisis,” says independent economist Lee Heng Guie.

The reasons for the fall in the ringgit this time is different.

The value of the ringgit was for some time after the peg was removed linked with the price of crude oil. As the price of crude oil rose, so the ringgit.

But as the price of crude oil collapsed like it has now, the ringgit felt the brunt. Political uncertainties in Malaysia is not helping the value of the ringgit.

The price of West Texas Intermediate is now at US$44.81 a barrel

The danger is what will happen to the real economy as the ringgit weakens?

The external trade sector will do well as seen in June’s export numbers. The steep decline of the ringgit in June lifted external trade by 5.0% year-on-year to RM64.3bil.

“In part, the weak ringgit currency spurred exports growth during the month. Ringgit fell to an average of RM3.74 per US dollar in June versus RM3.60 in May. Exports growth were driven by most export products except the exports of petroleum including crude petroleum, LNG and petroleum products. Primarily, the exports of E&E surged by 13.5% following two months of contractions,” says AmResearch in a note.

Although there are similarities in the movement of the ringgit between 1997/98 and today, the stark contrast was economic strength.

In 1997 Malaysia had a current account deficit and a fiscal surplus. That situation reversed a year later and has been so ever since.

The ringgit peg at RM3.80 afforded stability to exporters and that swelled the trade account in 1998. A fiscal deficit was realised after the Government embarked on priming, with the aid of lower government debt than today, to kickstart the economy which had been ravaged by a steep decline in economic activity.

One of the reasons why businesses found it hard going in 1998 was corporate leverage. A number of corporations were saddled with big debts and institutions such as Danaharta Nasional Bhd was formed to restructure corporate debt in Malaysia.

Conditions are reversed for most of corporate Malaysia today. Leverage has been kept in check and cash balances among corporates are in a far healthier state than it was in 1997/98.

The difference was also foreign reserves. From a high of US$34.6bil in May 1994, foreign reserves dropped to a low of US$17.5bil in 1997. Foreign reserves in Malaysia was US$96.7bil as at July 31.

Although the quantum of foreign reserves compared with the size of the economy is a comparative consideration, economists point out that the amount of reserves today is sufficient for nearly 7.6 months of imports. Back then, it was enough for just 3.2 months of imports.

“We have come a long way from the past. The banking system is well capitalised compared with back then,” says AmResearch economist Patricia Oh Swee Ling.

The biggest difference between 1997/98 and today are households.

During the Asian financial crisis almost two decades ago, household debt as a percentage of GDP was a meagre 16%.

At the end of last year, it was 87.9% and remains at an elevated level. The man in the street was generally immune to the crisis although there was an uptick in unemployment and higher loan repayments for loans as interest rates spiked.

While per capita income today is in excess of RM35,000 compared with RM12,314 in 1998, cost pressures have emerged. The goods and services tax (GST) has crimped spending power among consumers and retail sales, according to the Malaysia Retailers Association, contracted by 3% in the second quarter compared with a rise of 4.6% in the first quarter of 2015.

Purchasers by consumers has been a big factor in the growth of the economy and if private consumption, which accounts for 50% of GDP according to an economist, falls, then that will put pressure on economic growth in the second quarter.

Economic weakness ahead

Bank Negara will release second quarter GDP numbers next week and the general consensus is it will be lower than the first quarter. The consensus is for a growth of 4.5% for the second quarter.

Citigroup, in a note, projects second quarter GDP to come in at 4% compared with 5.6% in the first quarter.

“Services were dragged down by a 11.2% year-on-year plunge in motor vehicle sales post GST, while transport and utilities were also soft. Loan growth was stable, though fund raising in capital markets lifted financial services growth,” it says.

Citigroup says growth in mining slowed to below 8% from a year ago in the second quarter on weaker production volumes in gas and oil.

Manufacturing also slowed below 5% year-on-year on softer April-May electrical and electronic production, although rebounding in June to 7.1% year-on-year. Growth was likely cushioned by a turnaround in palm oil production and strong construction.

“From an expenditure perspective, the slowdown in second quarter GDP growth was likely led by domestic demand, especially consumption. We remain cautious on third quarter prospects given continued slump in the Composite Leading Indicator, second half growth should be cushioned by base effects, a gradual recovery from the GST induced slump, and a lift to manufactured exports from a US recovery,” it says.

Affin Hwang Capital believes that despite households adjusting to the GST following its implementation in early April, it believes private consumption will remain supportive of economic growth in the second half, supported by favourable labour market conditions on the back of steady increase in income and low unemployment rate in the country.

“Malaysia’s real GDP growth is expected to slow from 5.6% y-o-y in the first quarter to an estimated 4.5% in the second quarter, before recovering to an average of 5% y-o-y in the second half. We highlighted that our full year 2015 GDP forecast remained unchanged at 5% in 2015, at the mid-point of the official forecast of between 4.5% and 5.5% (6% in 2014).”

Moody’s Investors Service was more optimistic. It expects Malaysia’s economy to grow by 5.1% in the second quarter.

“Exports are the main drag, driven by soft global demand and low oil prices. This filters through to the domestic economy as unemployment rises and consumers reduce spending. Capital expenditure should remain buoyant as government infrastructure projects come on line.

Malaysia’s economy should pick up later this year as the global economy strengthens,” it says.

That scenario is a reality for Malaysian capital markets and the anxiety over a slowdown in China’s economy has got many worried about its effect on economic momentum in Malaysia.

Parallels from such a situation today can be drawn against what happened during the Asian Financial Crisis of 1997/98 but the setting is different than what happened almost 20 years ago.

Going back to 1997/98, it was a time when growth in Malaysia and South-East Asia was booming. Overheating worries turned into whether such growth was sustainable.

Starting with the attack on the Thai baht, the currencies of many South-East Asian countries were soon under attack.

The ringgit too felt the brunt of such attacks and at the worst, fell to RM4.80 to the dollar before recovering and ultimately pegged at RM3.80 to the dollar in September 1998.

“In 1997/98, it was contagion that caused problems. The currency crisis turned into a financial crisis,” says independent economist Lee Heng Guie.

The reasons for the fall in the ringgit this time is different.

The value of the ringgit was for some time after the peg was removed linked with the price of crude oil. As the price of crude oil rose, so the ringgit.

But as the price of crude oil collapsed like it has now, the ringgit felt the brunt. Political uncertainties in Malaysia is not helping the value of the ringgit.

The price of West Texas Intermediate is now at US$44.81 a barrel

The danger is what will happen to the real economy as the ringgit weakens?

The external trade sector will do well as seen in June’s export numbers. The steep decline of the ringgit in June lifted external trade by 5.0% year-on-year to RM64.3bil.

“In part, the weak ringgit currency spurred exports growth during the month. Ringgit fell to an average of RM3.74 per US dollar in June versus RM3.60 in May. Exports growth were driven by most export products except the exports of petroleum including crude petroleum, LNG and petroleum products. Primarily, the exports of E&E surged by 13.5% following two months of contractions,” says AmResearch in a note.

Although there are similarities in the movement of the ringgit between 1997/98 and today, the stark contrast was economic strength.

In 1997 Malaysia had a current account deficit and a fiscal surplus. That situation reversed a year later and has been so ever since.

The ringgit peg at RM3.80 afforded stability to exporters and that swelled the trade account in 1998. A fiscal deficit was realised after the Government embarked on priming, with the aid of lower government debt than today, to kickstart the economy which had been ravaged by a steep decline in economic activity.

One of the reasons why businesses found it hard going in 1998 was corporate leverage. A number of corporations were saddled with big debts and institutions such as Danaharta Nasional Bhd was formed to restructure corporate debt in Malaysia.

Conditions are reversed for most of corporate Malaysia today. Leverage has been kept in check and cash balances among corporates are in a far healthier state than it was in 1997/98.

The difference was also foreign reserves. From a high of US$34.6bil in May 1994, foreign reserves dropped to a low of US$17.5bil in 1997. Foreign reserves in Malaysia was US$96.7bil as at July 31.

Although the quantum of foreign reserves compared with the size of the economy is a comparative consideration, economists point out that the amount of reserves today is sufficient for nearly 7.6 months of imports. Back then, it was enough for just 3.2 months of imports.

“We have come a long way from the past. The banking system is well capitalised compared with back then,” says AmResearch economist Patricia Oh Swee Ling.

The biggest difference between 1997/98 and today are households.

During the Asian financial crisis almost two decades ago, household debt as a percentage of GDP was a meagre 16%.

At the end of last year, it was 87.9% and remains at an elevated level. The man in the street was generally immune to the crisis although there was an uptick in unemployment and higher loan repayments for loans as interest rates spiked.

While per capita income today is in excess of RM35,000 compared with RM12,314 in 1998, cost pressures have emerged. The goods and services tax (GST) has crimped spending power among consumers and retail sales, according to the Malaysia Retailers Association, contracted by 3% in the second quarter compared with a rise of 4.6% in the first quarter of 2015.

Purchasers by consumers has been a big factor in the growth of the economy and if private consumption, which accounts for 50% of GDP according to an economist, falls, then that will put pressure on economic growth in the second quarter.

Economic weakness ahead

Bank Negara will release second quarter GDP numbers next week and the general consensus is it will be lower than the first quarter. The consensus is for a growth of 4.5% for the second quarter.

Citigroup, in a note, projects second quarter GDP to come in at 4% compared with 5.6% in the first quarter.

“Services were dragged down by a 11.2% year-on-year plunge in motor vehicle sales post GST, while transport and utilities were also soft. Loan growth was stable, though fund raising in capital markets lifted financial services growth,” it says.

Citigroup says growth in mining slowed to below 8% from a year ago in the second quarter on weaker production volumes in gas and oil.

Manufacturing also slowed below 5% year-on-year on softer April-May electrical and electronic production, although rebounding in June to 7.1% year-on-year. Growth was likely cushioned by a turnaround in palm oil production and strong construction.

“From an expenditure perspective, the slowdown in second quarter GDP growth was likely led by domestic demand, especially consumption. We remain cautious on third quarter prospects given continued slump in the Composite Leading Indicator, second half growth should be cushioned by base effects, a gradual recovery from the GST induced slump, and a lift to manufactured exports from a US recovery,” it says.

Affin Hwang Capital believes that despite households adjusting to the GST following its implementation in early April, it believes private consumption will remain supportive of economic growth in the second half, supported by favourable labour market conditions on the back of steady increase in income and low unemployment rate in the country.

“Malaysia’s real GDP growth is expected to slow from 5.6% y-o-y in the first quarter to an estimated 4.5% in the second quarter, before recovering to an average of 5% y-o-y in the second half. We highlighted that our full year 2015 GDP forecast remained unchanged at 5% in 2015, at the mid-point of the official forecast of between 4.5% and 5.5% (6% in 2014).”

Moody’s Investors Service was more optimistic. It expects Malaysia’s economy to grow by 5.1% in the second quarter.

“Exports are the main drag, driven by soft global demand and low oil prices. This filters through to the domestic economy as unemployment rises and consumers reduce spending. Capital expenditure should remain buoyant as government infrastructure projects come on line.

Malaysia’s economy should pick up later this year as the global economy strengthens,” it says.

Source: The Star Online

Latest Posts

-

Industri hartanah perlu utamakan pemeliharaan ekologi - Nga

-

Treating homes as investments impedes affordability of homeownership

-

Radium labur RM135 juta bangun hotel 4 bintang di Chancery Ampang

-

KRI calls for housing finance overhaul as long loan tenures push up household debt risk

-

Projek KL360 @ Menara GD berjaya dipulihkan semula