News & Articles Malaysia's construction sector to keep growing

Malaysia's construction sector to keep growing

13 Jun 2016

AS the fairly strong momentum of project awards has been sustained in the last few years, the construction sector remained the fastest-growing economic sector in 2015. The sector’s GDP growth clocked in at 8.2% year-on-year (y-o-y), marginally lower than RAM’s forecast of 8.4%. Notably, the 10th Malaysia Plan drew to a close in 2015, with the construction sector charting a solid compound annual growth rate (CAGR) of 11% in the five-year period.

Moving forward, the RM260bil of development expenditure under the 11th Malaysia Plan (2016-2020) represents a 16% increase from the previous plan, which bodes well for the growth trajectory of the construction industry.

The value of construction work completed posted a circa 12% growth for a third consecutive year in 2015. An acceleration of civil engineering works had compensated for a tapering in the pace of growth in the property sectors. The cooling off in momentum was most evident in residential properties, which grew at 11% (2014: +22%), while construction work for non-residential properties recorded a 14% expansion (2014: +17%). Overall, these property segments still accounted for the lion’s share (more than 60%) of all construction activities (by value). For 1Q 2016, construction work advanced marginally lower at 11% y-o-y.

Despite the healthy overall industry growth, the 47 local listed construction companies (per RAM’s classification) delivered a mixed performance in 2015. These companies cumulatively generated RM3.6bil of pretax profit, with only slightly more than half of them (27 or 57%) charting a better y-o-y showing.

This highlights the volatility of earnings and the underlying execution risk faced by construction firms, particularly because they may have concentrated order books.

Construction firms have continued to enjoy favourable access to funding for their expansion. This was evinced by the healthy 12% CAGR for the banking system’s loans to the construction sector in the last three years. The bond market has also remained a viable funding avenue for construction players vis-à-vis financing diversity, with bonds/commercial papers forming at least 30% of the borrowings of RAM-rated construction firms. Outlook

We expect the high levels of project awards – of at least RM120 billion in the past two years – to further drive the construction sector’s growth. Amid the more challenging economic climate, however, the implementation of less urgent projects may be more uncertain – as implied from the recalibrated Budget 2016. For 1Q 2016, the GDP growth in the construction sector came in at 7.9%. RAM has retained its positive outlook on the construction sector this year, but expects GDP growth to ease slightly to 7.1%.

Prospects for the property segment have become more muted, with residential property sales in the primary market having eased and an oversupply facing the commercial property arena.

This could be offset by the award of headline-grabbing infrastructure jobs that have gained traction, with construction activity likely to be ramped up in 2H 2016.

The cumulative value of infrastructure project awards this year is expected to surpass the high of RM46bil in 2012, with momentum of awards gaining steam for rail and road projects. The biggest project to date is the RM32bil KVMRT Line 2, where seven major packages worth a combined RM22bil have been awarded.

In the pipeline, sizeable jobs undergoing the tender process include the LRT 3 and some highways. While oil-and-gas-related infrastructure job announcements are still flowing out of Pengerang, Johor, construction firms exposed to the upstream segment may face more challenges amid low oil prices and the scaling back of Petronas’ capital expenditure.

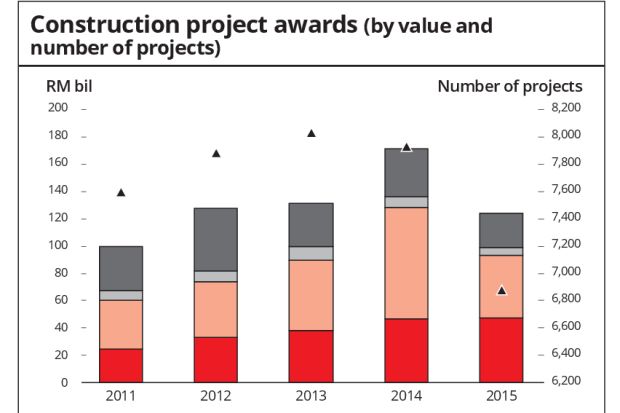

The order books of the 10 largest listed construction firms per RAM’s classification (by revenue) already offer sturdy multiples over their annual construction revenues. Most of these firms report a minimum coverage of 1.7 times, with IJM well ahead of the pack. Gamuda, on the other hand, enjoys fee-based income from its role as project delivery partner (PDP) for the KVMRT lines. Some of the jobs up for grabs this year, especially in the infrastructure segment, span several years, reducing the need for contractors to replenish work. However, order books for contractors will likely stay concentrated, underlining the importance of smooth job execution. In this regard, the value per project award for the past 2 years has grown to an average of RM20mil (see chart) from RM16mil in 2013.

The profitability of most listed construction firms is generally satisfactory, with only a handful of them boasting margins on earnings before interest, tax, depreciation and amorisation (EBITDA) of 30% or better.

While sector-wide operating profits still inched up in 2015, the recent upward revision in foreign worker levies in Peninsular Malaysia and the rise in steel bar prices since early 2016 – to some extent – are among main cost pressures crimping margins this year.

Companies with fixed-price contracts may feel more of the pinch unless the jobs are approaching their tail ends, or if they can be renegotiated.

In addition, the implementation of minimum wages effective July this year is likely to have a more pronounced effect on smaller firms as they have less flexibility in absorbing costs.

Source: DurianProperty.com

Latest Posts

-

Shah Alam Neighbourhood Spotlight: Why Auction Properties Here Are Worth a Second Look in 2026

-

Understanding the Proclamation of Sale (POS): What is a POS?

-

Jelajah Harta Tanah Malaysia 2026 Returns with Over 1,200 Property, Auto & Art Auction Opportunities

-

SD Guthrie and Sime Darby Property Advance Strategic Industrial Corridor into Next Phase

-

Industri hartanah perlu utamakan pemeliharaan ekologi - Nga